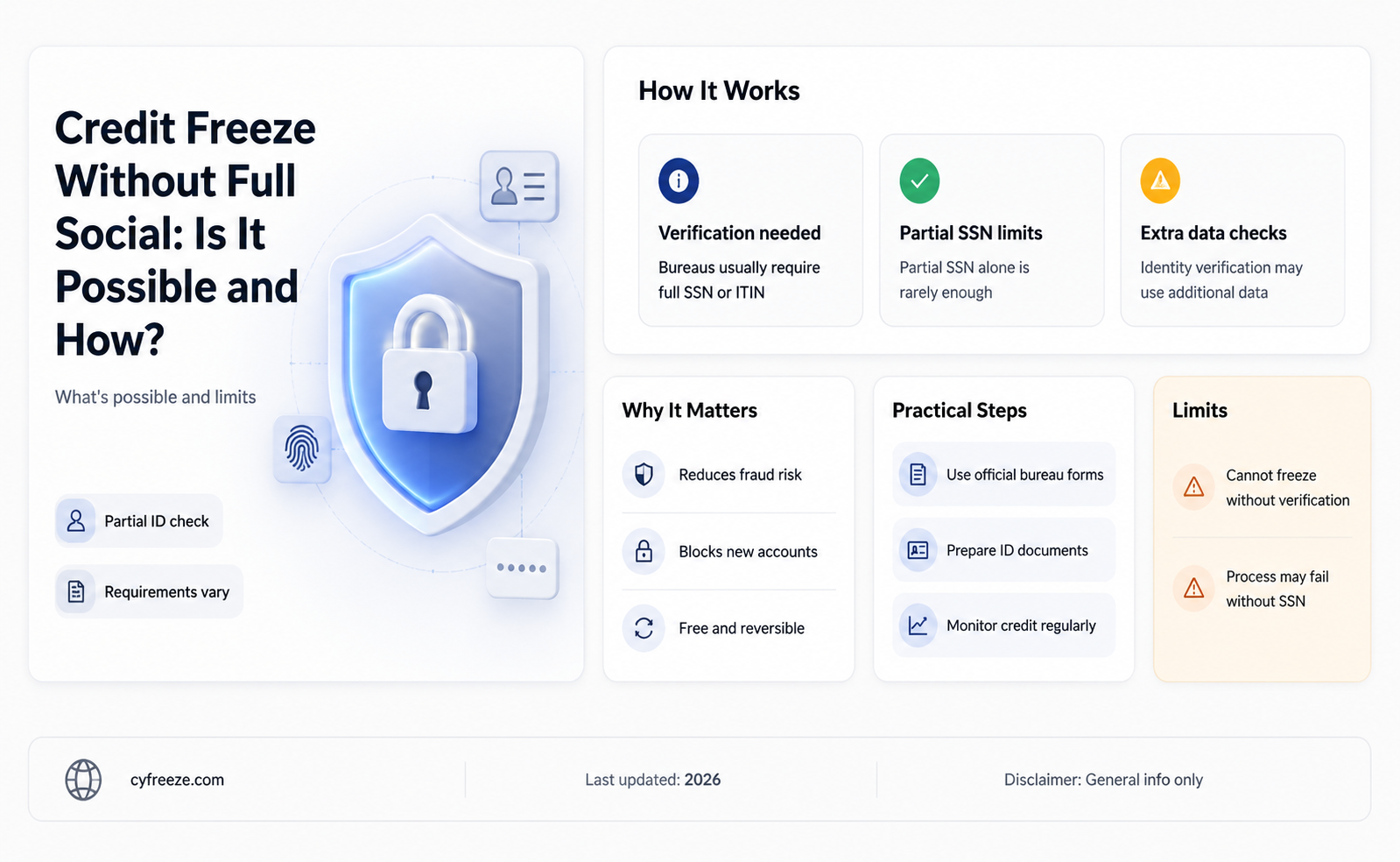

Obtaining a credit freeze is a crucial step in protecting your financial identity, but many wonder if it’s possible to do so without providing your full Social Security number (SSN). While most credit bureaus typically require your complete SSN to verify your identity and process the freeze, some may allow partial information or alternative forms of identification in certain circumstances. However, providing your full SSN is generally the most straightforward and secure method to ensure the freeze is applied correctly. If you’re hesitant to share your full SSN, it’s advisable to contact the credit bureaus directly to explore available options, such as using other personal details or documentation to verify your identity. Additionally, monitoring your credit reports and enrolling in fraud alerts can serve as temporary safeguards while you work through the process.

| Characteristics | Values |

|---|---|

| Full Social Security Number Required | Not always necessary; partial SSN or other identifying info may suffice. |

| Alternative Identification Methods | Driver's license, passport, or other government-issued ID. |

| Credit Bureau Policies | Varies by bureau (Equifax, Experian, TransUnion); some accept partial SSN. |

| Online Freeze Process | Often requires full SSN, but exceptions exist with additional verification. |

| Phone or Mail Requests | Higher chance of success with partial SSN and additional documentation. |

| State-Specific Laws | Some states allow freezes without full SSN under certain conditions. |

| Fraud Prevention Measures | Additional security questions or identity verification may be required. |

| Timeframe for Freeze | Immediate or within a few business days, depending on verification. |

| Cost | Typically free, as per federal law (e.g., Economic Growth, Regulatory Relief, and Consumer Protection Act). |

| Impact on Credit Score | No impact; credit freeze only restricts access to credit reports. |

Explore related products

What You'll Learn

- Partial Social Security Number Acceptance: Some agencies allow freezes with partial SSN verification for security

- Alternative Identity Verification Methods: Use driver’s license, passport, or utility bills to confirm identity

- Credit Bureau Policies: Equifax, Experian, TransUnion may have different SSN requirements for freezes

- Fraud Victim Exceptions: Victims of identity theft may freeze credit with limited personal information

- Third-Party Services: Some services assist in freezing credit without full SSN disclosure

![]()

Partial Social Security Number Acceptance: Some agencies allow freezes with partial SSN verification for security

In the realm of credit security, the Social Security Number (SSN) has long been the gold standard for identity verification. However, a growing trend among certain agencies is the acceptance of partial SSN verification for initiating credit freezes. This approach balances the need for security with the practical challenges consumers face in recalling or safely storing their full SSN. For instance, some credit bureaus and financial institutions now allow the use of the last four digits of an SSN, combined with other identifying information like a driver’s license number or date of birth, to verify identity. This method reduces the risk of full SSN exposure while still providing a robust security measure.

From an analytical perspective, the partial SSN acceptance strategy addresses a critical vulnerability in identity verification systems. Full SSNs are highly sensitive and, when compromised, can lead to severe identity theft. By requiring only a portion of the SSN, agencies minimize the potential damage from data breaches or phishing attempts. For example, if a hacker gains access to a database containing partial SSNs, the incomplete information is far less useful for fraudulent activities. This approach also aligns with the principle of data minimization, a best practice in cybersecurity that advocates collecting only the information necessary for a specific purpose.

For consumers, understanding how to leverage partial SSN acceptance can be a practical step toward protecting their credit. Here’s a step-by-step guide: First, contact your credit bureau or financial institution to confirm if they accept partial SSN verification for credit freezes. Second, gather the required supplementary information, such as your driver’s license number or recent account statements. Third, initiate the freeze request using the partial SSN and additional details. Be cautious, however, as not all agencies follow this practice, and some may still require a full SSN. Always verify the legitimacy of the agency and use secure communication channels to avoid scams.

A comparative analysis reveals that partial SSN acceptance is not universally adopted, creating a patchwork of practices across agencies. While some credit bureaus and banks have embraced this method, others remain hesitant due to concerns about verification accuracy. For instance, Experian and TransUnion have been more flexible in their SSN requirements compared to Equifax, which often insists on full SSN verification. This disparity highlights the need for standardized practices in the industry. Consumers should research and compare policies to identify which agencies offer the most convenient and secure options for their needs.

In conclusion, partial SSN acceptance represents a pragmatic solution to the challenges of credit security in an increasingly digital world. By reducing reliance on full SSNs, agencies enhance protection against identity theft while maintaining effective verification processes. For consumers, this trend offers a more manageable way to secure their credit without compromising safety. As this practice gains traction, it underscores the importance of staying informed about evolving security measures and advocating for policies that prioritize both convenience and protection.

Understanding Freezer Burn: Causes, Prevention, and How to Avoid It

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UL320_.jpg)

![]()

Alternative Identity Verification Methods: Use driver’s license, passport, or utility bills to confirm identity

Obtaining a credit freeze without a full Social Security number (SSN) is challenging but not impossible. When an SSN is incomplete or unavailable, alternative identity verification methods become essential. Among the most widely accepted are government-issued IDs like driver’s licenses or passports, which provide robust proof of identity through embedded security features and official databases. For instance, a driver’s license includes a unique number, photo, and expiration date, all of which can be cross-referenced with state records. Similarly, a passport carries international recognition and advanced anti-fraud measures, making it a highly credible verification tool. These documents serve as primary alternatives when traditional SSN-based methods fall short.

Utility bills, while less secure than government IDs, can also play a role in identity verification, particularly when combined with other documents. They establish residency and a link to the individual’s name, which is crucial for confirming identity in the absence of a full SSN. For example, a recent electricity or water bill with the applicant’s name and address can be paired with a driver’s license to create a layered verification process. However, utility bills are more susceptible to fraud, such as mail theft or digital manipulation, so they should never be used in isolation. Financial institutions often require at least two forms of verification when an SSN is incomplete, ensuring a higher level of confidence in the applicant’s identity.

Implementing these alternative methods requires careful consideration of their strengths and limitations. Driver’s licenses and passports are ideal for primary verification due to their official status and difficulty to counterfeit, but they may not always be available to applicants. In such cases, utility bills or bank statements can serve as secondary proof, though their reliability hinges on recent issuance and consistency with other provided information. For instance, a utility bill dated within the last 60 days is more credible than one from six months prior. Institutions must also ensure compliance with regulations like the Fair Credit Reporting Act (FCRA), which mandates reasonable procedures for verifying identity.

Persuasively, adopting these alternative methods not only addresses the challenge of incomplete SSNs but also enhances inclusivity in financial services. Individuals without a full SSN, such as recent immigrants or those with privacy concerns, can still access critical protections like credit freezes. By diversifying verification methods, institutions reduce reliance on a single identifier, which is increasingly vulnerable to breaches and fraud. For example, a combination of a passport and a utility bill can provide a more comprehensive identity profile than an SSN alone, especially in cases where the SSN has been compromised. This approach aligns with global trends toward multi-factor authentication and strengthens overall security.

In conclusion, alternative identity verification methods such as driver’s licenses, passports, and utility bills offer viable solutions for obtaining a credit freeze without a full SSN. Each method has distinct advantages and should be used strategically to compensate for the absence of traditional identifiers. Institutions must balance security, compliance, and accessibility, ensuring that verification processes are both robust and inclusive. Practical tips include verifying the authenticity of documents through official databases, cross-referencing multiple sources, and maintaining clear records of the verification process. By embracing these alternatives, financial systems can better serve diverse populations while safeguarding against identity fraud.

Can Frozen Marijuana Grow Mold? Storage Tips and Risks

You may want to see also

Explore related products

![Social Security Bible for Beginners: [2 in 1] Insider Tips To Maximize Benefits And Ensure A Secure Retirement | + A Workbook For Easy, Step-By-Step Guidance And Financial Planning Tools](https://m.media-amazon.com/images/I/71KiivjGQhL._AC_UL320_.jpg)

![]()

Credit Bureau Policies: Equifax, Experian, TransUnion may have different SSN requirements for freezes

Credit bureaus—Equifax, Experian, and TransUnion—are not monolithic entities with uniform policies. Each operates independently, and this extends to their requirements for placing a credit freeze, particularly when it comes to providing a Social Security Number (SSN). While all three bureaus require some form of identification to initiate a freeze, the specifics can vary, leaving consumers to navigate a patchwork of rules. For instance, one bureau might accept partial SSN information combined with other identifying details, while another may insist on the full nine-digit number. This inconsistency underscores the importance of understanding each bureau’s unique policies before attempting to freeze your credit.

To illustrate, let’s consider a hypothetical scenario. Imagine a consumer who has misplaced their SSN card but still wants to protect their credit. They might find that Experian allows them to proceed with a freeze using their name, address, and date of birth, provided they can answer security questions correctly. In contrast, Equifax could require at least the last four digits of the SSN, while TransUnion might demand the full number. These differences highlight the need for consumers to research each bureau’s requirements in advance, as failing to provide the necessary information could result in delays or denials.

From a practical standpoint, consumers should approach credit freezes strategically. Start by gathering all possible identifying information, including your full SSN, driver’s license number, and recent addresses. If you’re missing your full SSN, contact the bureaus directly to inquire about alternative verification methods. For example, some bureaus may accept a passport number or other government-issued ID in lieu of an SSN. Additionally, keep detailed records of your interactions with each bureau, including confirmation numbers and dates, to ensure accountability and streamline any follow-up actions.

A persuasive argument can be made for standardizing SSN requirements across all credit bureaus. Such uniformity would simplify the process for consumers, reduce confusion, and enhance security by ensuring consistent verification standards. Until that happens, however, individuals must remain vigilant and proactive. Advocate for yourself by staying informed about each bureau’s policies and leveraging available resources, such as online portals or customer service hotlines, to navigate the process effectively. Remember, a credit freeze is a powerful tool for protecting your financial identity, but its effectiveness depends on your ability to meet each bureau’s specific criteria.

In conclusion, while the goal of placing a credit freeze is universal, the path to achieving it varies depending on the bureau. By understanding and adapting to the unique SSN requirements of Equifax, Experian, and TransUnion, consumers can take control of their credit security with confidence. Treat each bureau as a distinct entity, prepare thoroughly, and approach the process with patience and persistence. Your financial well-being is worth the effort.

Freezer Burn on Meat: Can It Make You Sick?

You may want to see also

Explore related products

![]()

Fraud Victim Exceptions: Victims of identity theft may freeze credit with limited personal information

Victims of identity theft often face a Catch-22: their personal information has been compromised, yet they need that same information to protect themselves further. Fortunately, fraud victim exceptions exist, allowing individuals to freeze their credit even if they cannot provide their full Social Security number (SSN). This safeguard is critical because a credit freeze prevents new accounts from being opened in your name, effectively stopping fraudsters in their tracks.

To initiate a fraud victim exception, you typically need to provide alternative identifying information. This may include your name, address, date of birth, and a copy of a government-issued ID, such as a driver’s license or passport. Some credit bureaus may also accept a police report or an identity theft report from the Federal Trade Commission (FTC). While the process varies slightly between Experian, Equifax, and TransUnion, all three major bureaus recognize the urgency of protecting fraud victims and have streamlined procedures to accommodate limited information.

One practical tip is to contact the credit bureaus directly via their fraud-specific phone lines or online portals. For instance, Experian’s fraud assistance line can guide you through the process, ensuring your request is handled efficiently. Additionally, filing an FTC identity theft report not only strengthens your case but also provides a centralized document that all bureaus accept. Keep detailed records of all communications, including confirmation numbers and dates, as these can be invaluable if disputes arise later.

While this exception is a powerful tool, it’s not without limitations. For example, some state-specific requirements may apply, and processing times can vary. Moreover, a credit freeze doesn’t protect against all forms of fraud, such as misuse of existing accounts. Pairing a freeze with active monitoring and regular review of your credit reports maximizes your protection. For minors or dependents, guardians can request a freeze on their behalf, though additional documentation, like a birth certificate, may be required.

In conclusion, fraud victim exceptions offer a lifeline for those whose identities have been stolen. By understanding the process and preparing the necessary documentation, victims can take immediate action to safeguard their credit. While it’s a reactive measure, it’s a crucial step in reclaiming control and preventing further damage. Remember, acting swiftly and staying informed are your best defenses in the fight against identity theft.

Do Edibles Expire? Freezing Cannabis Treats for Longevity

You may want to see also

Explore related products

![]()

Third-Party Services: Some services assist in freezing credit without full SSN disclosure

For those wary of sharing their full Social Security Number (SSN) online, third-party services offer a compelling solution for initiating a credit freeze. These platforms act as intermediaries, leveraging alternative verification methods to confirm your identity and communicate with credit bureaus on your behalf. This approach minimizes direct exposure of your sensitive information while still achieving the desired outcome of protecting your credit.

Services like Privacy.com and Credit Sesame exemplify this model. They typically require only partial SSN information, combined with other identifying details such as your name, address, and date of birth. Some may even utilize knowledge-based authentication, posing questions about your financial history or public records to verify your identity. This multi-factor approach ensures security without relying solely on your full SSN.

It's crucial to exercise caution when selecting a third-party service. Research their reputation, privacy policies, and data security measures thoroughly. Look for established companies with a track record of transparency and positive customer reviews. Remember, you're entrusting them with sensitive information, so prioritize services that prioritize data protection.

While these services provide a valuable alternative, they often come with associated fees. Some charge a one-time fee for credit freeze assistance, while others operate on a subscription model offering ongoing credit monitoring and protection. Carefully evaluate the cost against the perceived risk of SSN exposure and your individual needs.

Ultimately, third-party services provide a viable option for individuals seeking to freeze their credit without disclosing their full SSN. By understanding their mechanisms, exercising due diligence in service selection, and weighing the costs, consumers can leverage these platforms to enhance their financial security while maintaining control over their sensitive information.

Can Popsicles Get Freezer Burn? The Chilling Truth Revealed

You may want to see also

Frequently asked questions

No, most credit bureaus require your full Social Security number to verify your identity and process a credit freeze request.

Yes, you can consider placing a fraud alert or using credit monitoring services, though these do not restrict access to your credit report as a freeze does.

No, credit bureaus typically require your full Social Security number to ensure accurate identification and prevent unauthorized freezes.

Your request will likely be denied, as the full SSN is a key requirement for identity verification in the credit freeze process.

Generally, no. Credit bureaus rely on your full Social Security number as the primary method of verification for credit freeze requests.