When considering whether you can freeze Medicare Part B after obtaining a job, it’s essential to understand the rules and options available. Medicare Part B, which covers outpatient services, typically requires enrollment during specific periods to avoid late penalties. If you return to work and gain employer-sponsored health insurance, you may be able to delay or suspend Part B without penalties, depending on the size of your employer and the coverage offered. However, this decision should be carefully evaluated, as gaps in coverage could lead to higher premiums later. Consulting with a Medicare specialist or your employer’s benefits coordinator can help clarify your options and ensure compliance with Medicare regulations.

| Characteristics | Values |

|---|---|

| Can Medicare Part B be frozen? | No, Medicare Part B cannot be "frozen" once enrolled. |

| Impact of getting a job on Part B | Getting a job does not allow you to freeze Part B. You remain enrolled. |

| Premiums while working | Part B premiums are still owed even if you have employer-based insurance. |

| Delaying Part B enrollment | Possible if you have credible employer-based coverage, but not a "freeze." |

| Penalty for late enrollment | Late enrollment penalties apply if Part B is delayed without valid reason. |

| Coordination with employer coverage | Employer coverage may become primary, but Part B remains active. |

| Withdrawal from Part B | Allowed only in specific circumstances (e.g., moving abroad). |

| Re-enrolling after leaving a job | Special Enrollment Period (SEP) available to avoid penalties. |

| Medicare Part B coverage | Continues regardless of employment status unless formally withdrawn. |

| IRS reporting requirements | Premiums may be tax-deductible; consult a tax professional. |

Explore related products

What You'll Learn

![]()

Eligibility for Medicare Freeze

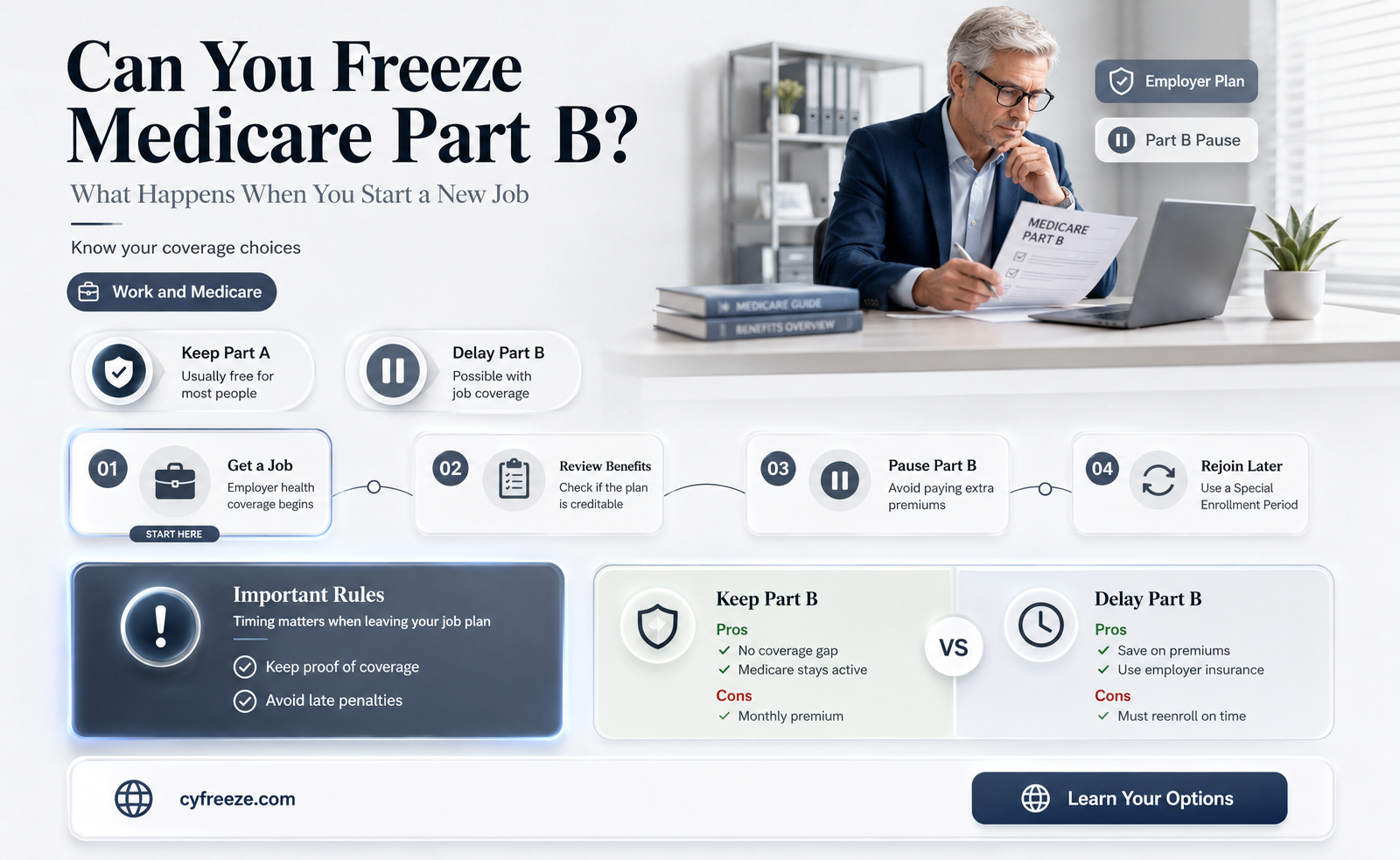

Medicare Part B, which covers outpatient services, is a vital component of healthcare for many Americans, particularly those aged 65 and older. However, life circumstances can change, and individuals may wonder if they can freeze their Medicare Part B coverage if they return to work. The concept of a "Medicare freeze" is not explicitly outlined in Medicare regulations, but there are specific scenarios where individuals can delay or adjust their Part B enrollment without penalties.

Eligibility Criteria for Delaying Part B Enrollment

If you return to work and have employer-sponsored health insurance, you may be eligible to delay enrolling in Medicare Part B without facing late enrollment penalties. This is particularly relevant if you are 65 or older and your employer’s coverage is considered "creditable," meaning it is at least as comprehensive as Medicare. For example, if you work for a company with 20 or more employees and have group health insurance, you can typically defer Part B until you retire or lose that coverage. It’s crucial to verify the creditability of your employer’s plan with your benefits administrator to ensure compliance with Medicare rules.

Steps to Delay Part B Enrollment

To delay Part B enrollment, follow these steps:

- Confirm Creditability: Obtain a written statement from your employer confirming that your health insurance is creditable.

- Decline Initial Enrollment: When you first become eligible for Medicare at 65, you can decline Part B enrollment by not signing up during your Initial Enrollment Period (IEP).

- Monitor Coverage Changes: If your employer coverage ends or changes, enroll in Part B during a Special Enrollment Period (SEP) to avoid penalties.

Cautions and Considerations

While delaying Part B can save you premiums, it’s essential to understand the risks. If you delay enrollment and your employer coverage is not creditable, you may face permanent late enrollment penalties, which increase your Part B premium by 10% for each 12-month period you were eligible but unenrolled. Additionally, if you have a Health Savings Account (HSA), enrolling in Part B will disqualify you from contributing to the HSA, even if you don’t use Medicare benefits.

Practical Tips for Navigating Part B Delays

If you’re considering delaying Part B, keep these tips in mind:

- Document Everything: Retain all correspondence with your employer and Medicare regarding your coverage decisions.

- Plan for Gaps: Ensure there’s no gap in coverage when transitioning from employer insurance to Medicare.

- Consult a Specialist: Speak with a Medicare advisor or SHIP (State Health Insurance Assistance Program) counselor to evaluate your specific situation.

By understanding the eligibility criteria and following these steps, you can make informed decisions about freezing or delaying Medicare Part B when returning to work.

Can Meat Get Freezer Burn? Causes, Prevention, and Safe Storage Tips

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UL320_.jpg)

![]()

Impact of Employment on Benefits

Employment status significantly influences Medicare Part B enrollment and premiums, particularly for individuals aged 65 and older who continue working. If you’re covered under an employer-sponsored health plan through your job or your spouse’s job, you can delay enrolling in Medicare Part B without penalties. This is because the employer’s group health plan acts as primary coverage, allowing you to defer Part B until you retire or lose that coverage. However, if the employer has fewer than 20 employees, Medicare becomes primary, and delaying Part B enrollment could result in late penalties. Understanding this interplay is crucial for avoiding unnecessary costs while maintaining adequate health coverage.

For those considering freezing Medicare Part B due to employment, the process involves strategic timing and documentation. If you’re working past 65 and have credible employer-based insurance, you can submit a request to delay Part B enrollment. This typically requires proof of current employment and health coverage, such as a letter from your employer or insurance provider. Once you retire or leave your job, you qualify for a Special Enrollment Period (SEP) to sign up for Part B without penalties. This SEP lasts for up to eight months after employment or group health plan coverage ends, providing a safety net for transitioning to Medicare.

A common misconception is that working automatically disqualifies you from Medicare benefits. In reality, employment can enhance your options by allowing you to delay Part B while maintaining comprehensive coverage. However, this strategy isn’t one-size-fits-all. For instance, if your employer’s plan has high out-of-pocket costs or limited provider networks, enrolling in Part B alongside it might offer better value. Conversely, if the employer plan is robust, delaying Part B could save you hundreds of dollars annually in premiums. Evaluating your specific health needs and financial situation is essential before making a decision.

Finally, consider the long-term implications of freezing Medicare Part B due to employment. While delaying enrollment can save money in the short term, it’s important to plan for the transition to Medicare as your primary coverage. Failing to enroll during your SEP could result in permanent premium increases of up to 10% for each 12-month period you were eligible but unenrolled. Additionally, if your employer coverage ends unexpectedly, having a clear understanding of Medicare enrollment timelines can prevent gaps in coverage. Proactive planning, such as consulting with a Medicare advisor or using online tools to compare plans, ensures a smooth transition when the time comes.

Can Your iPhone Survive the Freezer? Potential Damage Explained

You may want to see also

Explore related products

![]()

Reinstating Medicare Part B

Medicare Part B coverage isn't automatically lost when you return to work, but understanding reinstatement rules is crucial if you've previously dropped it. If you voluntarily terminated Part B due to employer-sponsored insurance, you generally qualify for a Special Enrollment Period (SEP) to reinstate it without penalties. This SEP lasts for eight months after your employer coverage ends or your employment stops, whichever happens first. Missing this window could mean paying higher premiums for late enrollment.

Key to reinstating Part B is contacting Social Security promptly. Provide proof of your previous Part B enrollment and documentation showing the end date of your employer coverage. This might include a letter from your employer or COBRA election notice. Acting quickly ensures seamless coverage and avoids gaps in healthcare access.

Unlike original enrollment, reinstating Part B doesn't require a waiting period for coverage to begin. Once your application is approved, your Part B coverage resumes the first day of the month following your request. This swift reinstatement is particularly beneficial if you've experienced a health change and need immediate access to Medicare-covered services.

Remember, reinstatement rules differ from initial enrollment. You're not subject to the general enrollment period (January 1 - March 31) with its associated late enrollment penalties. The SEP for reinstatement is your safety net, designed to protect individuals who temporarily relied on employer-based insurance.

While reinstating Part B is relatively straightforward, be mindful of potential pitfalls. Don't assume your employer will notify Social Security about your coverage changes. Take the initiative to contact them directly and provide all necessary documentation. Additionally, understand that reinstatement only applies to Part B. If you also dropped Part A, you'll need to re-enroll separately, potentially facing a waiting period. By proactively navigating the reinstatement process, you can ensure continuous Medicare coverage and avoid unnecessary financial penalties.

Brain Freeze: Unraveling Why You're Prone to the Icy Headache

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61wrmwXah3L._AC_UL320_.jpg)

![]()

Costs During Freeze Period

Freezing Medicare Part B when returning to work can save you money, but it’s not a cost-free decision. During the freeze period, you’ll no longer pay the Part B premium, which in 2023 is $164.90 per month for most beneficiaries. However, this savings comes with a trade-off: you’ll lose access to Medicare Part B coverage, which includes outpatient services like doctor visits, preventive care, and durable medical equipment. Before freezing, assess whether your new employer’s health insurance adequately replaces these benefits, as gaps in coverage could lead to out-of-pocket expenses for essential medical services.

One often-overlooked cost during the freeze period is the potential for penalties when you later reenroll in Part B. If you go without creditable coverage (insurance that meets or exceeds Medicare’s standards) for more than 8 months after your freeze ends, you’ll face a late enrollment penalty. This penalty is a 10% increase in your Part B premium for each 12-month period you were uninsured. For example, if you delay reenrollment by 2 years, your premium could rise by 20%, permanently. To avoid this, ensure your employer’s plan is creditable and document its coverage details.

Another hidden cost is the administrative burden of managing your healthcare transition. Freezing Part B requires coordination with both Medicare and your employer’s insurance provider. Mistakes in timing or paperwork can lead to coverage lapses or unexpected bills. For instance, if you freeze Part B but your employer’s plan hasn’t started, you could face a gap in coverage. Similarly, failing to notify Medicare when you return to work might result in continued Part B premiums being deducted from your Social Security benefits. Proactive communication and meticulous record-keeping are essential to avoid these pitfalls.

Finally, consider the opportunity cost of freezing Part B. While saving on premiums might seem appealing, Medicare Part B offers comprehensive coverage that many employer plans don’t fully replicate. For example, Medicare covers preventive services like flu shots and cancer screenings with no cost-sharing, whereas employer plans may require copays or deductibles. If you’re over 65 or have a chronic condition, losing access to these benefits could lead to higher out-of-pocket costs in the long run. Weigh the immediate savings against the potential risks before deciding to freeze your coverage.

Can Your Home Freezer Overheat in Hot Outdoor Conditions?

You may want to see also

Explore related products

![]()

Enrollment Rules Post-Freeze

Medicare Part B enrollment rules post-freeze are critical for individuals who return to work after a period of coverage suspension. Once you unfreeze Part B, you must reenroll during a Special Enrollment Period (SEP) if you meet specific criteria. This SEP typically lasts eight months after your employment or group health plan coverage ends, whichever occurs first. Missing this window could force you into the General Enrollment Period (January 1–March 31), resulting in late enrollment penalties and delayed coverage starting July 1.

To avoid penalties, understand the coordination between your employer’s group health plan and Medicare. If your employer has 20+ employees, their plan is primary, and you can delay Part B without penalty. However, if the employer has fewer than 20 employees, Medicare becomes primary, and freezing Part B without reenrolling post-freeze risks gaps in coverage. For example, a 67-year-old returning to a small business after freezing Part B must reenroll within eight months of leaving the job to maintain seamless coverage.

Practical steps include notifying your employer’s HR department when you plan to unfreeze Part B and contacting Social Security to initiate reenrollment. Documentation is key—keep records of employment end dates, group health plan coverage details, and reenrollment applications. If you’re unsure about eligibility, consult the Medicare Plan Finder tool or speak with a State Health Insurance Assistance Program (SHIP) counselor for personalized guidance.

Comparatively, reenrolling in Part B post-freeze is simpler than initial enrollment but requires vigilance. Unlike the Initial Enrollment Period (IEP), which is automatic for some, post-freeze reenrollment demands proactive steps. For instance, a 70-year-old who froze Part B while working full-time must act within the SEP to avoid penalties, whereas someone enrolling during their IEP faces no such hurdles. This distinction underscores the importance of understanding post-freeze rules to protect your healthcare continuity.

Finally, consider the financial implications. Late enrollment penalties for Part B are lifelong, adding 10% to your premium for each 12-month period you delayed enrollment. For someone with a $164.90 monthly premium in 2023, a 10% penalty increases costs by $16.49 monthly, or $197.88 annually. Multiply this over decades, and the cumulative cost becomes substantial. Thus, timely reenrollment post-freeze isn’t just about coverage—it’s about preserving long-term affordability.

Struggling to Obtain Mr. Freeze's Iconic Cryogenic Suit: A Guide

You may want to see also

Frequently asked questions

Yes, you can delay enrolling in Medicare Part B without penalty if you have credible health coverage through your employer or your spouse’s employer when you return to work.

No, as long as you enroll in Medicare Part B within eight months of losing your employer-sponsored coverage, you won’t face late enrollment penalties.

You don’t need to formally "freeze" Medicare Part B. Simply decline Part B when you first become eligible and keep documentation of your employer-sponsored coverage. When you’re ready to enroll, contact Social Security to sign up during a Special Enrollment Period.