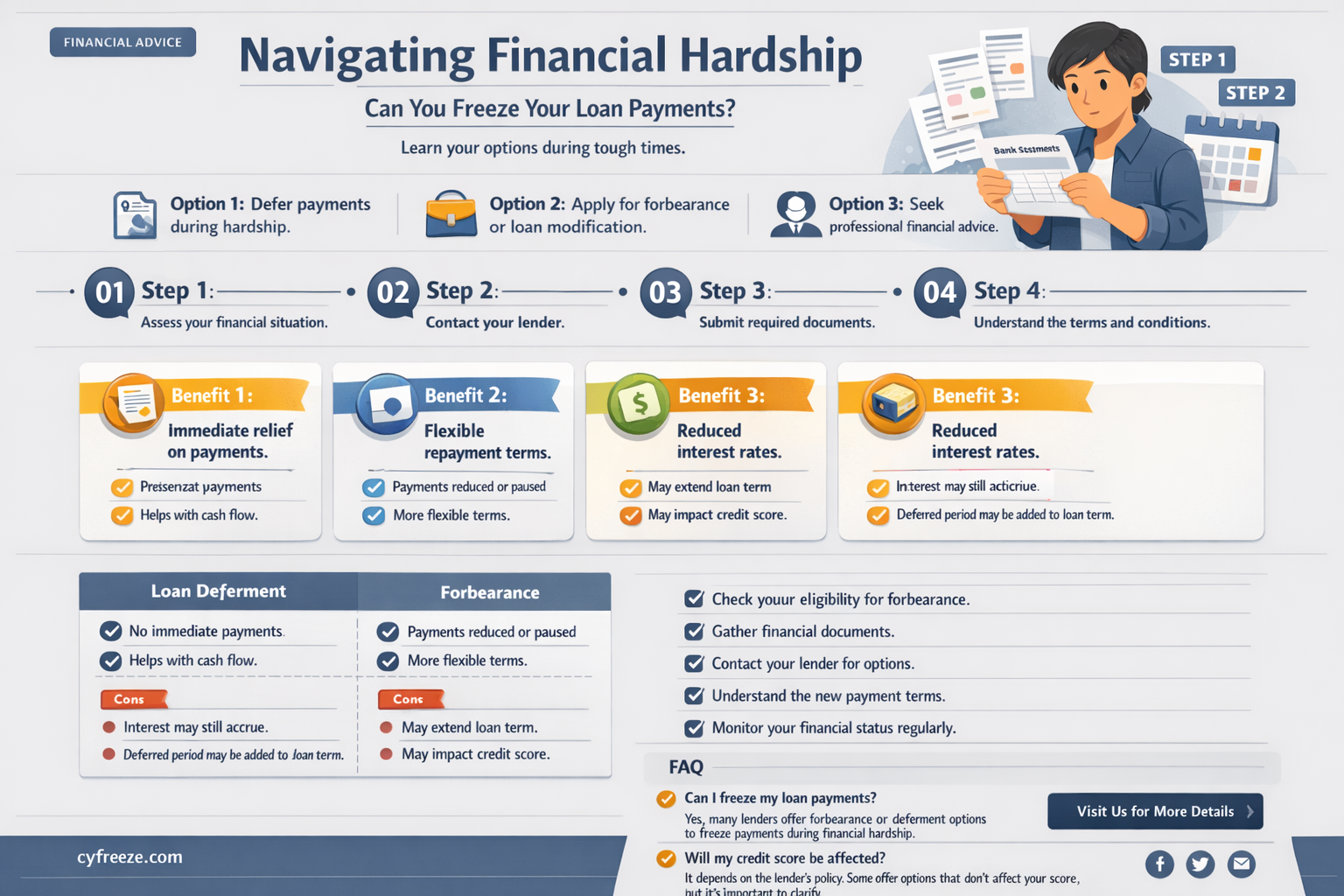

If you're struggling to make your loan payments, you may be wondering if it's possible to freeze your loan. Freezing a loan typically means temporarily suspending payments, which can provide some relief if you're facing financial difficulties. However, it's important to note that not all loans can be frozen, and the terms and conditions for doing so vary depending on the type of loan and the lender. In general, freezing a loan is more common for federal student loans, mortgages, and some personal loans. To determine if freezing your loan is an option, you'll need to contact your lender and discuss your situation. They may require documentation of your financial hardship and may have specific eligibility criteria to qualify for a loan freeze. Keep in mind that even if you're able to freeze your loan, interest may still accrue during the freeze period, which could increase the total amount you owe. Therefore, it's crucial to explore all available options and carefully consider the potential consequences before deciding to freeze your loan.

| Characteristics | Values |

|---|---|

| Loan Type | Federal student loans, private student loans |

| Conditions | Financial hardship, unemployment, health issues |

| Process | Contact lender, provide documentation, approval required |

| Duration | Temporary, varies by lender |

| Interest Accrual | May continue to accrue, varies by loan type |

| Credit Impact | May affect credit score, varies by loan type |

| Repayment Options | Resume payments when able, potential for loan forgiveness |

Explore related products

What You'll Learn

- Deferment Options: Explore temporary postponement of payments through deferment programs offered by lenders

- Forbearance Plans: Negotiate a forbearance agreement to pause payments temporarily due to financial hardship

- Loan Modification: Seek a permanent change to loan terms, such as interest rate or repayment schedule

- Refinancing Alternatives: Consider refinancing the loan to lower monthly payments or extend the repayment term

- Credit Counseling: Consult a credit counselor for personalized advice on managing debt and negotiating with lenders

![]()

Deferment Options: Explore temporary postponement of payments through deferment programs offered by lenders

Lenders often provide deferment programs as a temporary solution for borrowers who are unable to make their loan payments. These programs allow you to postpone your payments for a set period, which can be a lifesaver if you're experiencing financial difficulties. However, it's important to note that deferment doesn't forgive your debt; it simply delays the repayment.

To explore deferment options, you should first contact your lender to inquire about their specific programs. They may offer a variety of deferment plans, such as economic hardship deferment, unemployment deferment, or medical deferment. Each plan will have its own eligibility criteria and application process, so it's crucial to understand the details before applying.

When considering deferment, it's also important to weigh the potential benefits against the drawbacks. While deferment can provide immediate relief from your financial burden, it may also result in additional interest accruing on your loan. This could increase the total amount you owe in the long run. Furthermore, deferment may impact your credit score, as it could be viewed as a sign of financial distress.

If you decide to pursue deferment, be prepared to provide documentation to support your application. This may include proof of unemployment, medical records, or financial statements demonstrating your inability to make payments. The more thorough your application, the better your chances of approval.

Remember, deferment is a temporary solution, and it's essential to have a plan in place for when the deferment period ends. You may want to explore other options, such as loan modification or refinancing, to ensure you can manage your payments in the future. By understanding the ins and outs of deferment programs, you can make an informed decision about whether this option is right for you.

From Garden to Freezer: A Simple Guide to Making and Preserving Tomato Sauce

You may want to see also

Explore related products

![]()

Forbearance Plans: Negotiate a forbearance agreement to pause payments temporarily due to financial hardship

If you're facing financial hardship and struggling to make your loan payments, a forbearance plan could be a viable solution. Forbearance agreements allow borrowers to temporarily pause or reduce their loan payments for a specified period. This can provide much-needed relief during times of economic stress, such as job loss, medical emergencies, or natural disasters.

To negotiate a forbearance agreement, you'll need to contact your lender and explain your situation. Be prepared to provide documentation of your financial hardship, such as proof of unemployment, medical bills, or insurance claims. Your lender will review your request and may offer a forbearance plan that outlines the terms of the payment pause, including the duration and any conditions you must meet.

It's important to note that forbearance plans are not a long-term solution and should only be used as a temporary measure. During the forbearance period, interest may continue to accrue on your loan, which could increase the total amount you owe. Additionally, missed payments may negatively impact your credit score.

Before entering into a forbearance agreement, it's crucial to understand the terms and potential consequences. Consider consulting with a financial advisor or housing counselor to discuss your options and ensure you're making an informed decision. Remember, the goal of a forbearance plan is to provide temporary relief while you get back on your feet financially, not to indefinitely postpone your loan payments.

In conclusion, forbearance plans can be a helpful tool for borrowers experiencing financial hardship, but they should be approached with caution and a clear understanding of the terms and potential impacts on your financial situation.

The Surprising Culprit: How Dust Can Freeze Your PC

You may want to see also

Explore related products

![]()

Loan Modification: Seek a permanent change to loan terms, such as interest rate or repayment schedule

If you're struggling to make your loan payments, a loan modification could be a viable solution. This involves seeking a permanent change to your loan terms, such as a lower interest rate or a revised repayment schedule. Loan modifications can help make your monthly payments more manageable, potentially preventing foreclosure or default.

To pursue a loan modification, you'll need to contact your lender and explain your financial situation. Be prepared to provide documentation of your income, expenses, and any other relevant financial information. Your lender may require you to fill out an application and pay a fee to process your request.

There are several types of loan modifications available, depending on your specific needs and circumstances. For example, you may be able to secure a lower interest rate, which could reduce your monthly payment amount. Alternatively, you could request a longer repayment term, which would spread your payments out over a longer period of time, potentially lowering your monthly obligation.

It's important to note that loan modifications are not guaranteed, and your lender may deny your request. However, if you're facing financial hardship, it's worth exploring this option to see if you can find a more sustainable solution for your loan payments.

If you're considering a loan modification, it's a good idea to consult with a housing counselor or financial advisor to discuss your options and ensure you're making the best decision for your situation. They can help you understand the potential impact of a loan modification on your credit score and overall financial health.

Sweet Success: The Ultimate Guide to Freezing Homemade Fudge

You may want to see also

![]()

Refinancing Alternatives: Consider refinancing the loan to lower monthly payments or extend the repayment term

Refinancing a loan can be a viable strategy for individuals struggling to make their monthly payments. This process involves replacing the existing loan with a new one, potentially offering more favorable terms such as a lower interest rate, reduced monthly payments, or an extended repayment period. Before pursuing refinancing, it's essential to evaluate your financial situation and creditworthiness, as these factors will significantly influence the terms you can secure.

One approach to refinancing is to opt for a longer repayment term, which can lower your monthly payments by spreading the principal balance over a more extended period. However, this strategy may result in paying more interest over the life of the loan. Alternatively, if your credit score has improved since taking out the original loan, you may qualify for a lower interest rate, reducing both your monthly payments and total interest paid.

Another refinancing option is to switch from a variable-rate loan to a fixed-rate loan, providing stability and predictability in your monthly payments. This can be particularly beneficial if you anticipate rising interest rates in the future. Additionally, some borrowers may consider refinancing to remove a co-signer from the loan or to consolidate multiple debts into a single, more manageable payment.

It's crucial to weigh the potential benefits of refinancing against the associated costs, such as closing fees, appraisal fees, and prepayment penalties. Calculating the break-even point can help determine whether refinancing is a financially sound decision. Furthermore, borrowers should be cautious of predatory lending practices and thoroughly research potential lenders to ensure they are working with reputable institutions.

In conclusion, refinancing alternatives can offer relief to those struggling with loan payments, but it's essential to approach this strategy with careful consideration and a thorough understanding of the potential risks and rewards. By evaluating your financial situation, exploring different refinancing options, and working with reputable lenders, you can make an informed decision that aligns with your long-term financial goals.

From Chocolate Milk to Ice Cream: A Simple Freezing Trick

You may want to see also

![]()

Credit Counseling: Consult a credit counselor for personalized advice on managing debt and negotiating with lenders

Credit counseling can be a valuable resource for individuals struggling with debt and loan payments. A credit counselor can provide personalized advice on managing debt, creating a budget, and negotiating with lenders. They can also help individuals understand their credit reports and scores, and develop strategies to improve them.

One of the key benefits of credit counseling is that it can help individuals negotiate with lenders to reduce or freeze their loan payments. A credit counselor can act as an intermediary between the individual and the lender, helping to communicate the individual's financial situation and negotiate a mutually beneficial agreement. This can include reducing the interest rate, waiving fees, or temporarily suspending payments.

Credit counseling can also help individuals avoid common mistakes that can further damage their credit scores. For example, a credit counselor can advise against closing old credit accounts, which can negatively impact an individual's credit utilization ratio. They can also help individuals avoid debt settlement scams and other fraudulent schemes that can worsen their financial situation.

To get the most out of credit counseling, it's important to choose a reputable organization. Look for a credit counseling agency that is accredited by the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). These organizations have strict standards for their member agencies, ensuring that they provide high-quality, ethical services.

In conclusion, credit counseling can be a valuable tool for individuals struggling with debt and loan payments. A credit counselor can provide personalized advice, help negotiate with lenders, and guide individuals towards a more stable financial future. By choosing a reputable credit counseling agency, individuals can take the first step towards regaining control of their finances.

Silent Storage: The Truth About Zero-Noise Chest Freezers

You may want to see also

Frequently asked questions

Yes, under certain circumstances, you may be able to freeze your loan payments. This option is typically known as a loan deferment or forbearance. It allows you to temporarily stop making payments without defaulting on the loan. However, this is usually subject to specific conditions and approval from the lender.

During a loan deferment or forbearance, interest may continue to accrue on your loan balance. This means that even though you're not making payments, the total amount you owe could increase over time. It's important to check with your lender to understand how interest will be handled during this period.

Qualification for a loan deferment or forbearance typically depends on your financial situation and the terms of your loan agreement. Lenders may consider factors such as your income, expenses, and credit history. You may also need to provide documentation to support your request, such as proof of financial hardship or unemployment.

A loan deferment or forbearance itself may not negatively impact your credit score, as long as it's approved by the lender and you're not in default. However, it's important to continue making payments on other debts and financial obligations to maintain a positive credit history.

If you fail to make loan payments without an approved deferment or forbearance, you may default on the loan. This can lead to serious consequences, including damage to your credit score, collection calls, and potential legal action. It's crucial to communicate with your lender and explore available options if you're struggling to make payments.